CSRS Annuity Calculation Examples: Pros and Cons for Federal Employees

Key Takeaways

- CSRS annuities provide stable, predictable income but have limited portability and Social Security integration.

- Understanding calculation methods and scenarios empowers you to make informed federal retirement decisions.

If you’re a federal employee considering retirement or managing your plans for 2026, understanding how the Civil Service Retirement System (CSRS) annuity works is essential. Let’s break down its formulas, show real calculation examples, and walk through the benefits and drawbacks of this longstanding federal employee pension system.

What Is the CSRS Annuity?

History of CSRS for Federal Workers

The CSRS is a traditional defined benefit pension plan for U.S. federal employees. Established in 1920, CSRS was the primary retirement benefit for federal workers until it was replaced by the Federal Employees Retirement System (FERS) in 1987. While new hires now fall under FERS, many long-term employees and retirees still receive CSRS benefits.

How the Annuity Supports Retirement

The CSRS annuity provides monthly payments to eligible retirees based on their years of service and their high-three average salary. Unlike many private sector plans, it’s structured as a pension—offering steady income rather than a lump sum. This can help you cover living expenses throughout retirement.

Who Is Eligible for CSRS?

You qualify for CSRS if you were first hired as a federal employee before January 1, 1984, and did not opt into FERS. Eligibility generally requires a minimum number of years in service, with full benefits typically available to those who complete at least 30 years before the established age.

How Is the CSRS Annuity Calculated?

Basic Formula Explained

At its core, the CSRS annuity is calculated with a formula that considers your total years of creditable service and your high-three average salary. The high-three is the average of your highest-paid consecutive 36 months of basic pay.

The formula rewards longevity—the more years you work, the higher your annuity. It also encourages a full career in federal service but does allow for early, deferred, or partial service retirements with reduced calculations.

Key Factors in Calculation

A few important factors impact your CSRS annuity:

- Creditable service: Includes years, months, and even days spent working in eligible federal positions.

- High-three salary: Determined by averaging your highest three consecutive years of base pay.

- Unused sick leave: Can increase your creditable service time, boosting your benefit.

- Retirement age: Taking retirement before the standard age often reduces your calculation.

- Federal and state taxes: Are subtracted from your annuity, so consider net income in your planning.

What If You Have Military Service?

If you served in the military, those years can often be counted toward your federal service—if certain conditions are met. Typically, you must make a deposit to the retirement fund and satisfy rules about when your service occurred. Successfully including military service can increase your CSRS annuity calculation.

CSRS Annuity Calculation Examples for 2026

Scenario One: Full Career Employee

Suppose you worked as a federal employee for 35 years, retiring at age 62 in 2026. Your high-three salary is averaged over your highest consecutive 36 months. In this situation, your years of service and eligibility for unused sick leave credits mean your calculation will reflect a larger portion of your pay. The outcome is a stable monthly benefit, providing consistent retirement income for life.

Scenario Two: Early Retirement

Let’s say you are eligible for early retirement, with 25 years of service and retiring at age 55. The CSRS formula remains similar, but your benefit will be smaller than for a full career due to fewer years of service and your earlier retirement age. Additionally, reductions might apply, so your monthly payment will reflect a proportionate cut.

What Changes with Part-Time Service?

If you had part-time service during your federal career, your CSRS annuity calculation uses a prorated approach for those periods. The total creditable service is adjusted to reflect actual hours worked, and your high-three salary will also be weighted according to your scheduled hours during those years. This reduces the final benefit compared to full-time years but ensures even partial federal service counts toward your retirement.

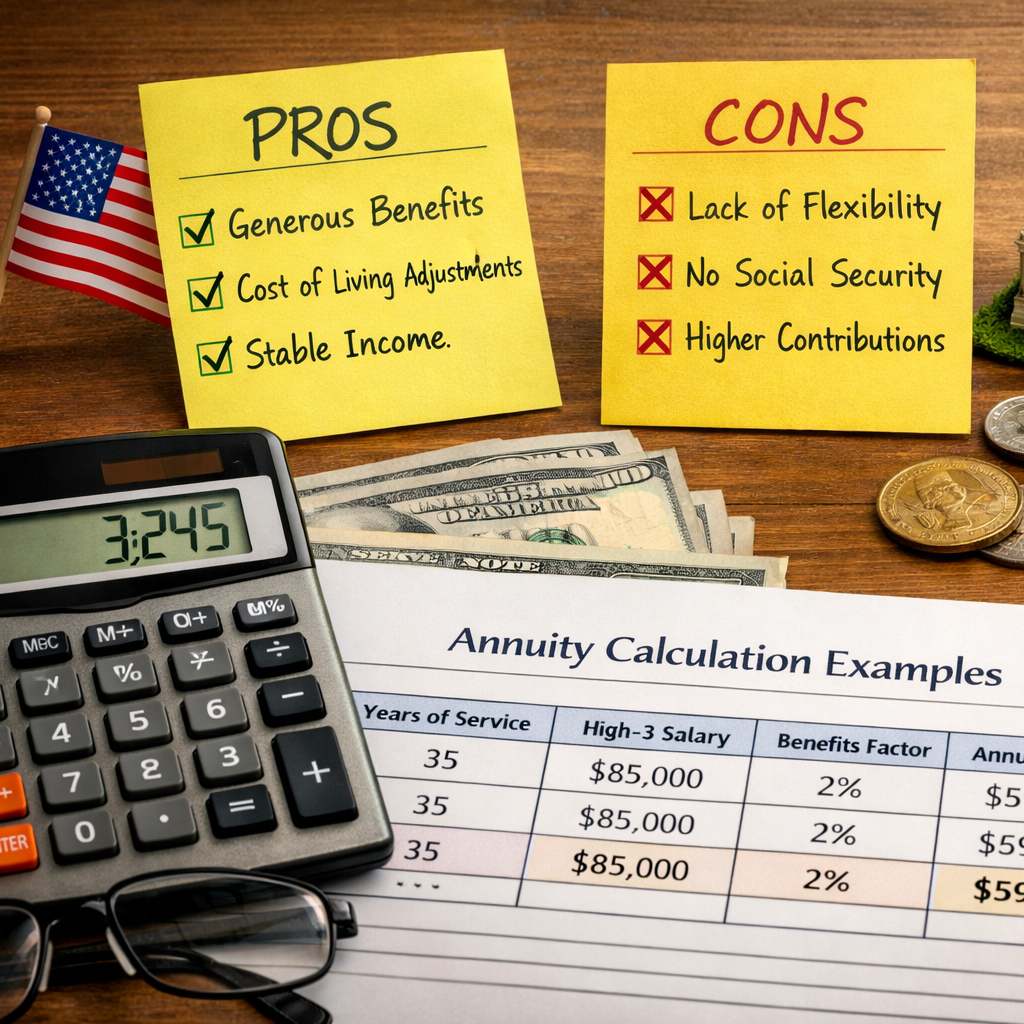

What Are the Pros of CSRS Annuities?

Stable Retirement Income

One of the most valued aspects of CSRS is its predictability. Each month, you receive a fixed benefit, helping you manage your budget and living expenses with less worry about market changes. This makes CSRS a reliable resource for federal retirees.

Cost-of-Living Adjustments

CSRS annuities offer cost-of-living adjustments (COLAs) most years. These adjustments help protect your purchasing power as the cost of everyday items goes up. While COLA percentages can vary, this feature supports your long-term financial well-being.

Long-Term Security Considerations

Unlike many private retirement plans, CSRS provides benefits for life. You don’t have to worry about funds running out, which can be reassuring when planning for retirement that could last decades.

What Are the Cons of CSRS Annuities?

Limited Portability

CSRS is tailored to federal employment. If you leave for a non-federal job, you cannot easily transfer your earned benefit to another employer’s plan. This makes the annuity less flexible for those who switch careers outside government service.

Lack of Social Security Integration

Most CSRS retirees do not pay into Social Security during their federal service, so they may receive little or no benefit from Social Security based on their government work. This means your retirement planning may need to account for a lack of Social Security coverage or the impact of rules like the Windfall Elimination Provision.

Potential Survivor Benefit Limitations

CSRS offers survivor benefits, but these options can come with restrictions. Generally, you must elect a reduced annuity to provide for a surviving spouse. Other limitations may affect benefits for children and dependents, so you should review your election choices carefully before retirement.

How Does CSRS Compare to FERS?

Key Differences for Federal Employees

The Federal Employees Retirement System (FERS) replaced CSRS for all new hires after 1983. FERS combines a smaller defined benefit pension with Social Security coverage and the Thrift Savings Plan (TSP), offering more diversified retirement income sources but a different benefit structure.

Which System Fits Your Needs?

If you are a CSRS-eligible employee, your focus will likely be on maximizing years of service and understanding your high-three salary. FERS participants may prioritize both pension and TSP contributions. For those with a choice between the two, factors like age, career length, and financial goals matter most.

Transition Considerations

CSRS employees had the option to switch to FERS in the late 1980s, but most current CSRS retirees or near-retirees chose to remain under the original system. If you’re considering any changes, carefully review eligibility and timing, as transitions between the systems are now rare and often irreversible.

Popular posts

COLA Rules for FERS...

Key Takeaways FERS and...

CSRS Eligibility: Requirements, Pros...

Key Takeaways CSRS is...

Free Retirement Benefits Analysis

Federal Retirement benefits are complex. Not having all of the right answers can cost you thousands of dollars a year in lost retirement income. Don’t risk going it alone. Request your complimentary benefit analysis today. Get more from your benefits.

I want more