Why Updating Your Beneficiary Designations Matters More Than Your Will in Protecting Your Retirement Assets

Key Takeaways

- Timely review and update of beneficiary designations is essential to ensuring your assets pass smoothly to intended recipients.

- Beneficiary forms often override wills, making accuracy and maintenance of these forms a top priority in estate planning.

Making sure your beneficiary designations are current can be one of the most important steps you take in managing your retirement plans. Many people overlook these crucial forms, risking confusion or disputes for their loved ones. This article will walk you through what beneficiary designations are, why mistakes occur, and how you can avoid common pitfalls to protect your legacy.

What Are Beneficiary Designations?

Definition and purpose

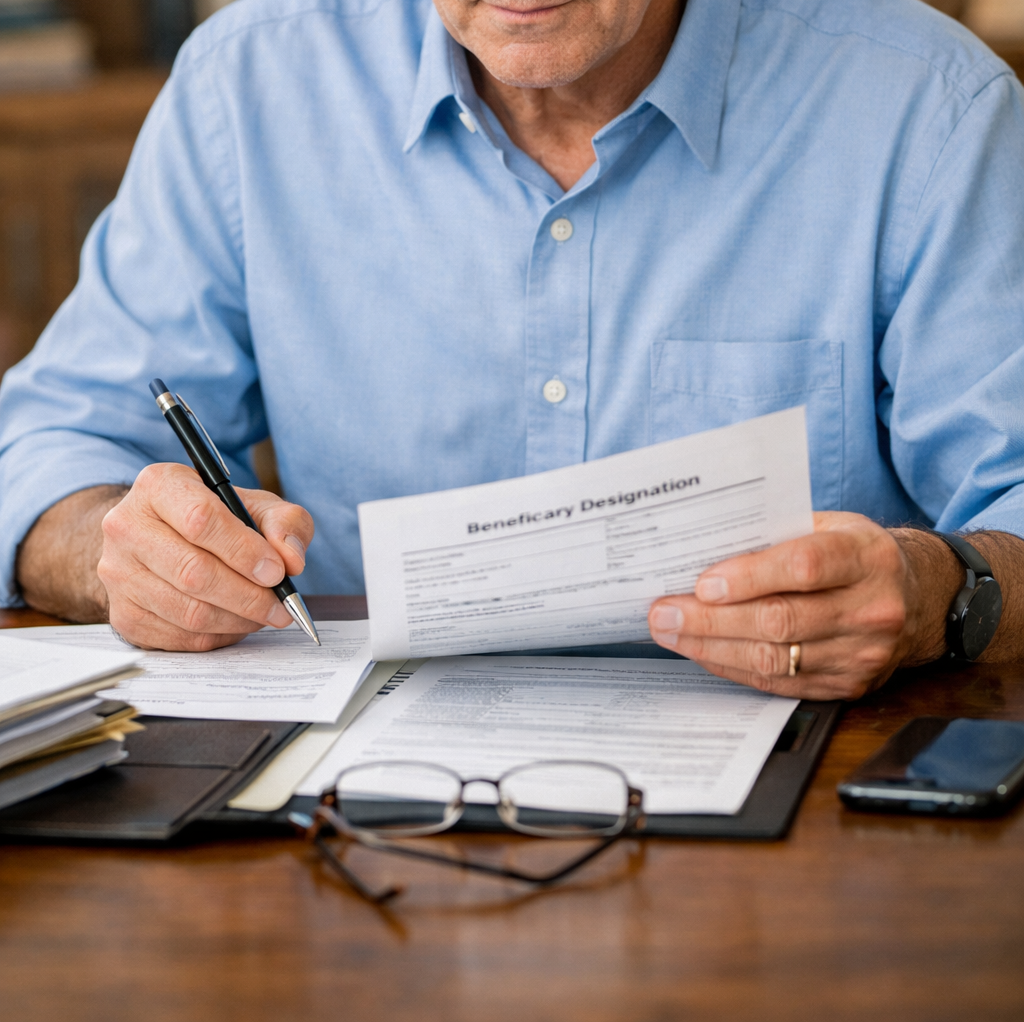

A beneficiary designation is a legal instruction telling account administrators who should receive your account assets after your death. When you fill out a beneficiary form for a retirement, banking, or insurance account, you’re choosing who inherits its balance. These designations bypass probate, allowing a smoother, faster transfer of assets directly to your chosen person or entity.

Types of accounts that require designations

You’ll encounter beneficiary forms with several types of accounts. These usually include retirement plans such as the Thrift Savings Plan (TSP), individual retirement accounts (IRAs), and workplace 401(k)s. Life insurance policies, annuities, and some brokerage accounts also require you to name beneficiaries. Understanding which accounts you own that demand a beneficiary designation is the first step in making sure everything is aligned with your wishes.

Why Do Beneficiary Mistakes Happen?

Misunderstanding account requirements

Many people assume all financial accounts work the same way, but beneficiary requirements often vary. For example, some plans default to a spouse if no beneficiary is named, while others may require documentation or ignore your will’s instructions. A lack of clarity in plan rules or a misunderstanding about how beneficiary rules work can cause costly errors.

Overlooking life event changes

Major life changes are often overlooked. Marriage, divorce, the birth or adoption of a child, or the loss of a loved one can all mean your old beneficiary instructions no longer match your intentions. It’s easy to forget to make updates during these busy or stressful times, but an outdated designation often overrides your will or other instructions.

How Can You Avoid Common Errors?

Review deadlines and documentation

Each retirement plan and insurance provider has its own rules and timelines for updating beneficiaries. Be aware of documents you need—such as marriage licenses, divorce decrees, or proof of guardianship—if you want to change a designation. Stay ahead by reviewing documents and forms soon after any big life event or at least once every few years.

Double-check details on beneficiary forms

Small clerical mistakes can sometimes lead to large problems. For example, an incorrect Social Security number or misspelled name could delay or even invalidate your designation. When filling beneficiary forms, check every field for accuracy. Confirm the full name, date of birth, and relationship of each person or entity. Keeping a signed copy of the final form for your records is a smart practice.

What Happens If You Don’t Update?

Consequences of outdated beneficiaries

If your beneficiary records are outdated, the account or policy may pay out to someone you no longer intend—such as a former spouse or a deceased individual. This can inadvertently disinherit children, new partners, or charities you care about. In some cases, accounts with no living primary beneficiary might default to your estate, causing delays and extra costs for those you leave behind.

Potential impact on loved ones

Confusing or outdated records can lead to disputes between family members, legal challenges, and emotional stress at an already difficult time. Timely and clear beneficiary updates mean your savings, insurance, and pension benefits reach those you wish to support, shielding loved ones from unnecessary complications.

Are Beneficiary Forms Stronger Than a Will?

How designations compare to wills

Beneficiary forms typically take legal priority over your will. This means if you name one person as a beneficiary on file with your retirement plan or insurance provider, and your will says something different, the plan administrator must follow the beneficiary form. It’s important to keep beneficiary forms in sync with the latest version of your will to avoid unintended outcomes.

Role of other legal documents

Other legal documents, like living trusts or power of attorney, serve vital roles in estate planning—but usually do not override a properly completed beneficiary form. You should coordinate all your planning documents so they work together, not against each other. Consulting with an estate planning attorney can help clarify how these instruments interact.

Steps to Update Your Beneficiaries

Gather all account information

Start by listing every account and policy you own that allows or requires a beneficiary choice. This might include workplace retirement accounts, personal life insurance policies, and investment accounts. Check each institution’s process for updating, since forms and requirements may vary.

Notify your human resources or plan administrator

For workplace plans, contact your human resources office or plan administrator when you want to make a change. They can give you the correct forms and guide you through any needed documentation. Make sure you receive confirmation when changes are accepted and processed.

Should You Consider a Trust as Beneficiary?

Benefits and drawbacks of trusts

Naming a trust as a beneficiary can provide more control over how your assets are distributed after your death. Trusts are useful if you want to direct funds for a specific purpose or for minor children, or to manage complex family circumstances. However, trusts come with setup and maintenance costs, and instructions must be very clear to avoid confusion or delays.

When trust designations may fit

Trusts may be appropriate if your beneficiaries are not able to manage large sums of money themselves, or if you have blended family structures and want to avoid direct beneficiary conflicts. If you’re considering this option, it’s wise to consult a legal or financial professional familiar with federal retirement and benefits planning.

How Often Should You Review Designations?

Key times to revisit beneficiaries

Plan to review all your beneficiary designations after any major life event—marriage, divorce, a birth or adoption, or a death in the family. Even if nothing seems to have changed, doing an annual check-up ensures your intentions are still reflected.

Using checklists to stay updated

Maintaining an estate planning checklist, including dates of your last updates, can be helpful. You might set a recurring reminder or align your review with tax season each year. This habit can give you and your loved ones peace of mind knowing everything is current and accurate.

Popular posts

Why Updating Your Beneficiary...

Key Takeaways Timely review...

Coordinating the FERS Supplement...

Key Takeaways Understanding how...

Free Retirement Benefits Analysis

Federal Retirement benefits are complex. Not having all of the right answers can cost you thousands of dollars a year in lost retirement income. Don’t risk going it alone. Request your complimentary benefit analysis today. Get more from your benefits.

I want more

Other Betty Morales Articles

COLA Rules for FERS vs CSRS: Key Differences in Federal Retirement Increases

Key Takeaways FERS and CSRS retirement systems have distinct COLA eligibility requirements and calculation methods for federal retirees. Knowing how...

READ MORE

Comparing Federal Retirement Planners vs Generalists: Myths vs Facts

Key Takeaways Federal retirement planners offer unique expertise tailored to public sector benefits. Understanding planner qualifications and asking the right...

READ MORE

Q&A: Bucket Strategy Using TSP and Cash Reserves for Public Sector Retirees

Q&A: Bucket Strategy Using TSP and Cash Reserves for Public Sector Retirees Key Takeaways Using your TSP and cash reserves...

READ MORE

Building a Retirement Plan for Federal Couples: Best Practices and Strategies

Key Takeaways Coordinating federal retirement benefits as a couple can unlock greater financial security and flexibility. Evaluating pension, healthcare, and...

READ MORE